What happens when you realize the driver who hit you only carries the Texas state minimum of $30,000, but your emergency room visit alone cost more than that? It is a terrifying reality that many face in 2026, especially with nearly 20% of drivers on our roads operating without sufficient coverage. If you are feeling stuck between rising medical costs and an insurance adjuster who has suddenly stopped acting like a "good neighbor," you aren't alone. Partnering with a dedicated underinsured motorist lawyer Texas is often the only way to ensure your recovery isn't cut short by someone else's poor financial choices.

You deserve to focus on healing without the constant shadow of debt hanging over your family. We understand that filing a claim against your own policy can feel like a betrayal of your loyalty, but it is actually the execution of a contract you paid for to protect your future. This guide will show you how to secure maximum compensation by tapping into your UIM policy for lost wages and long-term medical needs. We will explain how to hold negligent drivers accountable and why pursuing these benefits is a vital step toward your total restoration.

Key Takeaways

- Understand why the 30/60/25 Texas insurance minimums are often insufficient to cover serious medical costs in 2026.

- Learn how an experienced underinsured motorist lawyer Texas helps you access your own UIM policy when the other driver's coverage falls short.

- Identify the common tactics insurance companies use to devalue claims, including the "adversarial" shift in your own provider's behavior.

- Discover the essential steps for gathering evidence and reporting a claim to ensure your long-term healing is fully funded.

- See how a battle-tested professional uses corporate-level rigor to advocate for your holistic restoration and long-term financial stability.

The Crisis of Underinsured Drivers on Texas Roads in 2026

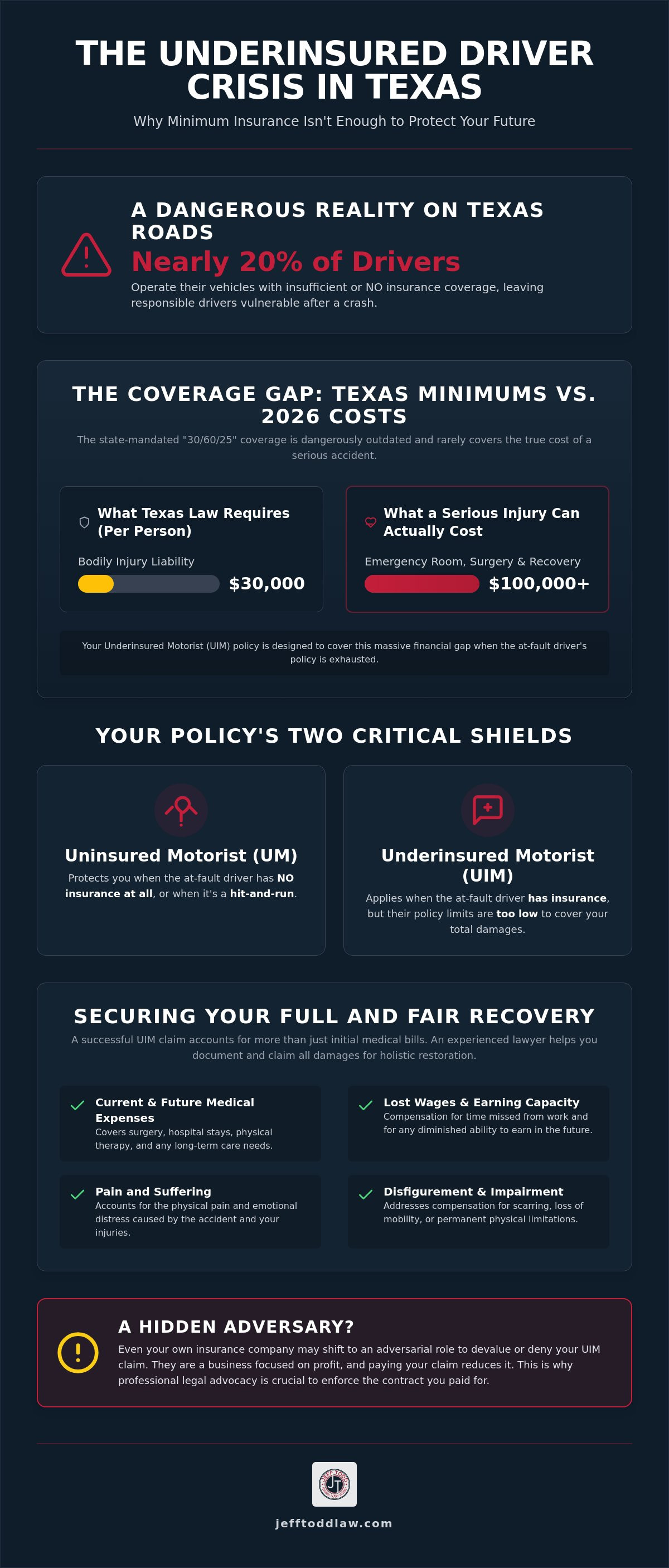

A typical Tuesday morning on I-10 in Houston or I-35 in Austin can change in a heartbeat. You're following the law, paying your premiums, and staying alert. Then, a sudden impact leaves you with a totaled vehicle and a mounting stack of medical bills. The shock of the crash is often followed by a second, deeper blow. You discover that the person who hit you doesn't have enough insurance to cover your recovery. In 2026, this isn't just a rare occurrence; it's a systemic crisis on Texas highways.

Recent data from April 2026 indicates that approximately 20% of Texas drivers are operating vehicles without any insurance at all. Even more concerning are the millions of drivers who carry only the bare minimum required by law. When you're facing a long road to physical restoration, discovering that a negligent driver is "judgment proof" or underinsured creates an immense emotional burden. It feels like a second victimization. This is why partnering with an experienced underinsured motorist lawyer Texas is essential to bridge the gap between a meager policy limit and your actual financial needs.

UIM vs. UM: Knowing the Difference

Understanding your policy starts with distinguishing between two critical types of coverage. An Uninsured motorist clause (UM) protects you when the at-fault driver has no insurance at all or flees the scene in a hit-and-run incident. Conversely, Underinsured Motorist (UIM) coverage applies when the other driver has a policy, but their limits are too low to pay for your total damages. Both are vital tools that Houston car accident lawyers use to evaluate the full scope of a client's available recovery options. Without these protections, you could be left responsible for costs you didn't cause.

Why "Minimum Coverage" is a Trap for Texas Families

Texas law currently mandates a 30/60/25 minimum limit. This provides $30,000 for bodily injury per person, $60,000 total per accident, and $25,000 for property damage. While this makes a driver "legal" to be on the road, it rarely makes them financially responsible in the face of 2026 medical inflation. A single complex surgery or a few days in a specialized trauma center can easily exceed $30,000 before you even consider your lost wages or the cost of future rehabilitation. Underinsured Motorist coverage serves as a vital contractual safety net that provides compensation for damages that exceed the at-fault party’s available insurance limits. Relying on a skilled underinsured motorist lawyer Texas ensures that you aren't left footing the bill for someone else's decision to carry the bare minimum.

Decoding Texas Insurance Minimums: Why $30,000 is Rarely Enough

Texas law requires drivers to carry liability insurance, but the minimum limits often fail to provide a true safety net. The current 30/60/25 rule means $30,000 for bodily injury per person, $60,000 for bodily injury per accident, and $25,000 for property damage. In a 2026 economic environment, these figures are dangerously low. Surgical costs in Houston and Austin have risen sharply. A single orthopedic procedure can consume a $30,000 limit before the patient even leaves the recovery room. When medical inflation outpaces these static legal requirements, the "financially responsible" driver is often anything but.

Consider a multi-car pileup on the Loop 610 or the Mopac Expressway. If three people are injured, that $60,000 "per accident" limit is split between them. Each victim might only receive $20,000, regardless of the severity of their trauma. This is where the Stowers Doctrine becomes relevant. It places a duty on insurance companies to act reasonably when a settlement offer within policy limits is made. If they fail to protect their insured, they may face consequences; however, for you, the victim, the primary concern remains the massive financial gap. An underinsured motorist lawyer Texas can help you identify these gaps early and determine if your own policy must step in.

Calculating Your Total Damages

Recovery is about more than just the immediate hospital bill. It includes lost wages, future earning capacity, and the profound impact of pain and suffering. We work with expert witnesses who project these long-term "holistic healing" costs to ensure your settlement reflects reality, not just the current balance on your credit card. You should never sign a release from an insurance adjuster until your Houston personal injury lawyer has evaluated the full scope of your injuries. Once you sign, you lose the right to seek further compensation, even if your condition worsens.

Texas Department of Insurance (TDI) Protections

The Texas Department of Insurance has rules to protect you. Insurers must offer UM/UIM coverage in writing. If you never signed a formal rejection letter, Texas law often applies a "Default Coverage" rule. This means you might have protection you didn't even know existed. Jeff Todd meticulously investigates policy documents to find these hidden layers of coverage. If you suspect your insurance company is withholding information about your available benefits, reaching out to a knowledgeable legal advocate can help reveal the truth.

The Hidden Adversary: Why Your Own Insurer May Fight Your UIM Claim

Filing a claim with your own insurance company feels like a safe bet. You've paid your premiums for years, expecting loyalty in return. However, the moment you initiate an Underinsured Motorist (UIM) claim, the relationship shifts from cooperative to adversarial. In the eyes of the law, your insurer essentially steps into the legal shoes of the negligent driver. They aren't looking out for your total restoration anymore; they're looking to protect their bottom line. Considering that national data shows approximately one in seven drivers, were uninsured or underinsured, these claims are frequent, and insurers have developed sophisticated playbooks to devalue them.

You might encounter adjusters who suddenly question the necessity of your treatment or attribute your pain to pre-existing conditions from years ago. This is a standard tactic designed to reduce the settlement value. The "good neighbor" persona often vanishes when a high-value claim is filed. Understanding these corporate strategies requires an underinsured motorist lawyer Texas who has seen the industry from the inside. Whether your accident involved a vehicle or a complex premises liability issue, your carrier's goal is to minimize subrogation losses and keep their payouts low.

The "Consent to Settle" Requirement

A frequent and devastating mistake victims make is settling with the at-fault driver's insurance company before notifying their own UIM carrier. If you accept a check and sign a release without your insurer's written permission, you may inadvertently waive your right to access your UIM benefits. Texas law requires specific notice to your UIM carrier before finalizing a third-party settlement to preserve your right to additional recovery. This simple procedural slip can cost you hundreds of thousands of dollars in much-needed funds for long-term healing.

Bad Faith Claims in Texas

Sometimes, an insurer's behavior crosses the line from aggressive defense to legal violation. Under Chapter 541 of the Texas Insurance Code, you're protected against unfair settlement practices and bad faith denials. If your company refuses to pay a valid claim without a reasonable basis, they may be held liable for additional damages. Jeff Todd uses his extensive corporate-legal background to anticipate these defensive maneuvers. He applies the same intellectual rigor used by elite firms to hold insurers accountable to the contracts they signed with you.

Step-by-Step: Pursuing a UIM Claim After a Texas Car Accident

The moments following a collision are chaotic, but they are also the most critical for your legal protection. While your priority is physical safety, the actions you take at the scene lay the foundation for your future financial recovery. You must build a body of evidence that an underinsured motorist lawyer Texas can use to prove both the other driver's liability and the true extent of your damages. This process begins with a formal police report and immediate medical documentation, even if your injuries seem minor at first. Internal trauma often masks itself behind adrenaline, only revealing its full cost days or weeks later.

When you report the accident to your own insurance carrier, stick to the facts. Don't admit fault or speculate on the cause of the crash. Your goal is to establish a clear medical paper trail that links the incident directly to your long-term restoration needs. You should trigger your UIM coverage as soon as it becomes clear that your medical bills and lost wages will exceed the at-fault driver's policy limits. Navigating these overlapping layers of insurance requires precision to ensure you don't accidentally waive your rights to the very benefits you've paid to maintain.

Evidence That Wins UIM Cases

Modern litigation in 2026 relies heavily on digital evidence. We look for dashcam footage, witness statements captured on video, and data from electronic data recorders (EDRs) that track speed and braking patterns. For specialized cases, such as those involving a motorcycle accident attorney, we often use 2026 crash reconstruction technology to demonstrate how an underinsured driver's negligence caused catastrophic harm. This high-tech approach provides the intellectual rigor necessary to counter an insurer’s attempt to devalue your claim.

The Statute of Limitations and Deadlines

Time is a silent adversary in personal injury law. In Texas, you generally have two years from the date of the crash to file a lawsuit for bodily injury. However, UIM claims are unique because they are rooted in contract law. While the statute of limitations for a breach of contract claim is typically four years from the date the insurer denies the claim, you shouldn't delay. Waiting for a medical malpractice attorney Texas to clear your health or hoping for a voluntary settlement can result in missed notice requirements. Most policies require "prompt notice" of a potential UIM claim, and failing to provide this can jeopardize your entire recovery. If you're concerned about missing these critical windows, contact our team today to review your policy deadlines.

Why Jeff Todd is the Battle-Tested Choice for Texas UIM Victims

Success in a UIM claim requires more than just filling out forms; it demands a deep understanding of how insurance companies protect their bottom line. Jeff Todd has been licensed since 1994, giving him over three decades of experience within the Texas legal system. He spent years in elite corporate environments, learning the exact strategies adjusters use to devalue claims. Today, The Todd Law Group, PLLC uses that intellectual rigor to advocate for individuals in Houston, Austin, and Galveston. Partnering with an underinsured motorist lawyer Texas who understands the opposition's playbook is the most effective way to secure the compensation you need for a full recovery.

Our firm is built on the principle of holistic restoration. We don't just see you as a case number; we see a person whose life has been disrupted by someone else's negligence. This commitment to your well-being is why we operate on a contingency fee basis. You don't face any upfront legal fees or out-of-pocket costs. We only receive payment if we successfully recover money for you, allowing you to focus on your physical healing while we handle the complex litigation and insurance negotiations.

Local Presence in Houston, Austin, and Galveston

Regional expertise matters when you are dealing with the court systems in Harris, Travis, or Galveston County. Our team provides the personalized attention of a local practice with the sophisticated resources of a major metropolitan firm. This specialized knowledge is particularly valuable in complex commercial wrecks, where our experience as a Houston truck accident lawyer helps us uncover every potential layer of UIM coverage. We ensure that no stone is left unturned in your pursuit of justice.

Take the First Step Toward Restoration

The journey toward your total recovery begins with a single, no-risk conversation. During your consultation, we will evaluate your policy documents and provide a clear roadmap for your claim. We handle every interaction with the insurance adjusters, shielding you from their high-pressure tactics. You deserve a stable partner who is personally invested in your community and your future. Schedule your free consultation with The Todd Law Group, PLLC today.

Secure Your Future Restoration Today

You shouldn't have to bear the lifelong financial weight of someone else's decision to carry inadequate insurance. The $30,000 Texas minimum is a legal baseline that rarely addresses the reality of 2026 medical inflation or the long-term impact of lost wages. Whether you were struck on a busy Houston highway or a local Austin street, your path to total restoration depends on holding every available policy accountable. By tapping into your UIM benefits, you are simply executing a contract you've already paid for to protect your family's future stability.

Partnering with a seasoned underinsured motorist lawyer Texas ensures that your own insurance company treats your claim with the seriousness it deserves. Jeff Todd has been licensed since 1994 and applies elite corporate-legal rigor to help individuals navigate these adversarial proceedings. With offices in Houston, Austin, and Galveston, we provide localized, battle-tested advocacy on a contingency fee basis. This means you face zero upfront costs while we fight for your recovery. Contact Jeff Todd for a Free UIM Case Review today. You deserve a partner who is committed to your holistic healing and financial peace of mind.

Frequently Asked Questions

Will my insurance rates go up if I file an underinsured motorist claim in Texas?

Texas law generally prohibits insurance companies from increasing your premiums for claims where you were not at fault. Since a UIM claim is based on the negligence of another driver, your insurer shouldn't penalize you for using the protection you've paid for. It's helpful to have an underinsured motorist lawyer Texas review your policy to ensure your carrier follows these state regulations during the settlement process.

Can I sue an underinsured driver personally if their insurance isn’t enough?

You have the legal right to sue the negligent driver personally, but this is often not the most effective path to recovery. Drivers who carry only the minimum state limits frequently lack the personal assets necessary to pay a large judgment. These individuals are often considered "judgment proof." Tapping into your own UIM policy is usually the most reliable way to secure funds for your long-term healing and financial restoration.

What is the difference between uninsured and underinsured motorist coverage?

Uninsured coverage (UM) protects you when the at-fault driver has no insurance at all or flees the scene in a hit-and-run. Underinsured coverage (UIM) triggers when the other driver has a policy, but their limits are too low to cover your total medical bills and lost wages. Both are essential safety nets that work together to ensure your physical and financial recovery isn't stalled by another driver's choices.

How much UIM coverage should I carry on my Texas auto policy?

You should carry as much UIM coverage as you can reasonably afford, ideally matching your own liability limits. While the state minimum is $30,000, this rarely covers the costs of a complex surgery or an extended hospital stay in 2026. Carrying higher limits, such as $100,000 or $250,000, provides a much stronger foundation for your family’s security if you are involved in a serious collision on a Texas highway.

Does UIM coverage pay for my car repairs or just my medical bills?

Underinsured coverage is typically split into two distinct parts: Bodily Injury (UIMBI) and Property Damage (UIMPD). The bodily injury portion covers your medical expenses, pain and suffering, and lost income. The property damage portion pays for your vehicle repairs or replacement. If you're confused about your specific policy limits, an underinsured motorist lawyer Texas can help you interpret your declarations page to identify all available avenues for recovery.

What happens if I was a passenger in a car involved in an underinsured accident?

As a passenger, you are generally covered by the UIM policy of the vehicle you were riding in at the time of the impact. If those limits aren't enough to cover your injuries, you may also be able to access the UIM benefits on your own personal auto policy. This process can be legally complex, but it is a vital step in ensuring your medical bills are fully funded without depleting your savings.

Can I still file a UIM claim if I was partially at fault for the accident?

Texas uses a modified comparative negligence rule, which means you can still recover damages as long as you aren't more than 50% responsible for the crash. Your final settlement will be reduced by your percentage of fault. For example, if you are 10% at fault, you can still recover 90% of your total damages. We focus on proving the other driver's primary negligence to maximize your available recovery.

How long does a UIM settlement take to process in Texas?

The timeline for a UIM claim depends on the length of your medical treatment and the complexity of the evidence. You shouldn't finalize a settlement until you have reached maximum medical improvement to ensure all future costs are included. Once your demand is submitted, the Texas Insurance Code requires insurers to follow specific deadlines for acknowledging and investigating your claim, which helps keep the process moving toward a resolution.