Did you know that 14.44% of vehicles in Harris County currently lack verified insurance coverage? In a high-traffic city like ours, this means every commute carries the risk of a collision with an irresponsible driver. If you've been hit by someone without a policy, filing an uninsured motorist claim Houston is often the only viable path to cover your medical bills and vehicle repairs. It's a stressful realization to find that your own insurance company may now become your legal opposition in your pursuit of justice.

You're likely worried about rising premiums or the weight of mounting debt while you're trying to heal. We understand that this process feels more like a legal battle than a recovery. This guide provides a strategic roadmap to help you secure maximum compensation even when the at-fault driver has no assets. You'll learn how to navigate complex Texas UM/UIM laws, hold your insurer accountable to their promises, and find the peace of mind that comes with a total restoration of your health and finances in 2026.

Key Takeaways

- Discover why nearly 20% of local drivers are currently uninsured and how this reality impacts your ability to recover damages after a crash.

- Learn the essential "24-Hour Protocol" for reporting incidents to the Houston Police Department to protect your legal right to a claim.

- Understand how to successfully navigate an uninsured motorist claim Houston even when your own insurance company takes an adversarial stance against you.

- Explore the holistic healing model that prioritizes both your physical restoration and your financial stability through expert medical coordination.

- Gain a clear understanding of the differences between UM and UIM coverage to ensure you are utilizing every available resource in your policy.

The Reality of Uninsured Motorist Accidents in Houston

Houston is a city defined by its scale and its speed. With millions of vehicles traversing our expansive freeway system every day, the statistical probability of an accident is high. However, the nature of these accidents has shifted significantly as we move through 2026. A standard collision is difficult enough to manage, but when the at-fault party lacks coverage, the situation transforms from a logistical headache into a full-scale legal crisis. If you find yourself in this position, pursuing an uninsured motorist claim Houston is no longer just an option; it's a necessary step toward protecting your future.

The psychological impact of these incidents is often as heavy as the physical damage. There is a profound sense of injustice when you realize the person who caused your injuries has zero assets and no accountability. This isn't just about a damaged bumper. It's about the fear that your own financial stability will be sacrificed because of someone else's negligence. Understanding the uninsured motorist clause in your own policy is the first step in reclaiming control over your recovery process.

Why Houston's Uninsured Rate Remains a Critical Concern

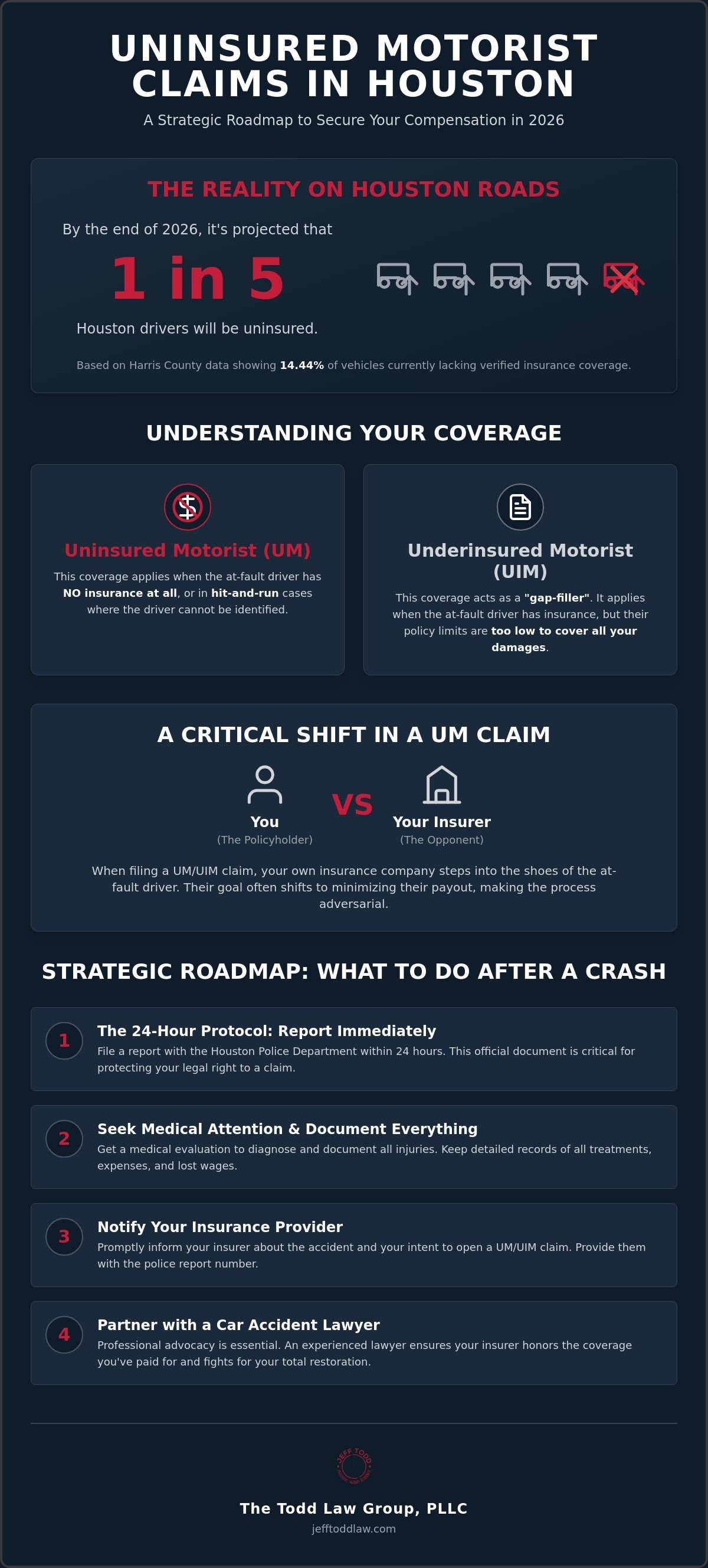

Economic pressures in 2026 have created a perfect storm for Houston drivers. As insurance premiums in Texas have climbed by over 50% since 2022, many individuals are forced to choose between groceries and auto coverage. In Harris County, data shows that roughly 14.44% of vehicles lack verified insurance, but this number often spikes in high-density urban areas. By the end of 2026, the convergence of record-high premiums and urban density is projected to leave nearly one in five Houston drivers operating without any liability coverage.

Traffic "Hot Spots" only exacerbate this risk. If you frequent the West Loop or the Southwest Freeway, you're navigating some of the most congested and high-risk corridors in the state. The sheer volume of traffic in these zones increases the frequency of UM/UIM incidents, leaving responsible drivers vulnerable to the financial fallout of a "no-insurance" crash.

The Financial and Physical Toll of a No-Insurance Collision

When the other driver can't pay, the burden shifts immediately to your shoulders. You're suddenly facing medical deductibles, emergency room fees, and the cost of vehicle repairs that can easily reach five figures. These are just the immediate hurdles. Long-term recovery often involves lost wages from missed work and the daunting expense of ongoing physical rehabilitation. Without a clear strategy, these costs can lead to a cycle of debt that hinders your holistic healing.

This is where professional advocacy becomes essential. A seasoned Houston car accident lawyer acts as a bridge between your current distress and total restoration. We don't just look at the police report; we look at the totality of your needs, ensuring that your own insurance company honors the coverage you've faithfully paid for. You shouldn't have to navigate the aftermath of a collision alone when the system feels stacked against you.

Understanding UM/UIM Coverage in Texas

Your insurance policy serves as a critical safety net when the unexpected happens on Houston roads. When you file an uninsured motorist claim Houston, you're essentially asking your own insurance provider to step into the shoes of the at-fault driver. This coverage isn't a luxury; it's a foundational component of a holistic restoration strategy that prioritizes your physical and financial health over corporate profits. It ensures that a single incident doesn't derail your entire life.

Data from the Insurance Information Institute previously indicated that approximately one in seven drivers were uninsured nationwide. In a sprawling metropolis like ours, that risk is even more pronounced due to high traffic density and rising premium costs in 2026. UM/UIM coverage is your primary defense against the economic devastation that often follows a major collision, especially when the other party lacks the means to take accountability.

UM vs. UIM: Knowing the Difference Before You File

Understanding the distinction between these two components is vital for your recovery. Uninsured Motorist (UM) coverage applies when the at-fault driver has no insurance at all or in hit-and-run cases where the driver cannot be identified. Underinsured Motorist (UIM) coverage acts as a gap-filler. If the other driver carries only the Texas state minimum of $30,000 for bodily injury, but your medical bills reach $100,000, your UIM coverage provides the remaining $70,000 needed for your care. You can find these limits listed clearly on your insurance declarations page, usually directly under your liability limits.

Texas Requirements: Is UM Coverage Mandatory?

Texas law operates on a principle of consumer protection regarding these coverages. Under the Texas Insurance Code, insurers must offer UM/UIM coverage to every policyholder. If you didn't specifically sign a written rejection form, the law presumes you have this coverage at the same limits as your liability policy. In Texas, there's a legal presumption that you carry UM/UIM coverage unless your insurer can produce a signed document proving you waived it. While the state-mandated minimum is 30/60/25, we often recommend higher limits to account for the rising costs of medical care in 2026. If you're struggling to understand your specific policy language, consulting a personal injury advocate can provide the clarity you need to move forward with confidence.

Viewing your claim through a holistic lens means recognizing that financial recovery is a prerequisite for physical healing. You can't focus on rehabilitation if you're drowning in medical debt. By securing the full value of your UM/UIM policy, you create the stable environment necessary for a total and lasting recovery.

The Adversarial Nature of UM Claims: When Your Insurer Becomes the Opponent

Many policyholders are surprised to find that when they initiate an uninsured motorist claim Houston, the relationship with their insurance provider shifts from supportive to adversarial. You've likely viewed your insurance company as a stable partner, but in the context of a UM claim, they effectively step into the shoes of the at-fault driver. This creates a fundamental conflict of interest. Your insurer's primary objective is to protect their financial reserves, which often means finding reasons to minimize or deny your payout. In this legal environment, your own insurance carrier becomes the defendant.

Don't be misled by a "friendly" claims adjuster who reaches out with an early settlement offer. While they may appear helpful, their role is to gather evidence that devalues your claim before the full scope of your medical needs is established. At The Todd Law Group, PLLC, we understand these corporate maneuvers from the inside. Jeff Todd leverages his elite corporate defense background to anticipate insurer tactics, ensuring that the same high-stakes rigor used by major firms is applied to your personal recovery. According to Texas law on uninsured motorist coverage, these protections are your right, but you need a dedicated advocate to ensure they're honored.

Common Tactics Used to Deny or Devalue Your Houston UM Claim

One of the most common devaluing strategies is the request for a recorded statement. Adjusters use specific phrasing to nudge victims into admitting partial fault or suggesting that their pain is less severe than it truly is. Additionally, insurers may dispute the "Physical Contact" rule in hit-and-run cases, questioning whether an impact actually occurred to avoid liability. They may also use intentional delays, hoping that the pressure of mounting medical bills will force you to accept a lowball offer out of desperation. These tactics are designed to exhaust your patience and your finances.

The Bad Faith Risk: Holding Your Insurance Company Accountable

Insurance companies have a legal obligation to handle claims fairly. When an insurer denies a valid claim without a reasonable basis or fails to investigate properly, they may be acting in bad faith. In Texas, legal principles like the Stowers Doctrine exist to protect policyholders from insurers who refuse to settle within policy limits when liability is clear. If your provider is employing deceptive tactics, it's critical to consult a seasoned Houston personal injury lawyer to hold them accountable. This level of advocacy is essential for maintaining the integrity of your holistic healing process and ensuring your total restoration remains the priority.

A Strategic Roadmap: What to Do After a Hit-and-Run or Uninsured Crash

The moments following a collision are often chaotic and disorienting. However, your actions during this initial window serve as the foundation for your uninsured motorist claim Houston. If you're hit by a driver who flees the scene or admits they lack coverage, your priority must be safety, followed immediately by meticulous documentation. You shouldn't assume the insurance company will take your word for it weeks later. By following a structured roadmap, you protect your legal rights and set the stage for a successful recovery.

The 24-Hour Rule: Reporting Requirements for Hit-and-Run Victims

Many victims are unaware that Texas insurance policies often include a strict 24-hour reporting requirement for hit-and-run incidents. If you wait longer than this to notify the Houston Police Department, your insurer may have grounds for an automatic denial of your claim. If HPD officers are unable to respond to the scene due to high call volume, you must still file an official report. You can use the Texas Driver's Crash Report (CR-2), commonly known as a "Blue Form," to document the event for the state. While you're at the scene or shortly after, look for witnesses and check for nearby doorbell cameras. This footage is often overwritten within days, so securing it immediately is vital for proving the occurrence of the crash.

Evidence Gathering: Building a Case Without an At-Fault Insurer

Since there's no opposing insurance company to investigate the scene, you must act as your own advocate. Take tactical photos from multiple angles, capturing vehicle damage, skid marks on the pavement, and surrounding street signs or traffic lights. Identifying the point of impact is essential because it proves how the collision occurred and prevents your insurer from shifting blame onto you. A timely, detailed police report serves as the indispensable anchor for your entire recovery process.

Beyond the accident scene, your medical records become the most significant evidence in your case. Insurers look for "gaps in treatment" to argue that your injuries weren't serious or were caused by a separate event. We recommend maintaining a "Healing File" that tracks your symptoms daily, organizes every medical bill, and logs the specific hours you've missed from work. This organized approach supports our holistic healing model by providing a clear narrative of your journey toward restoration. If you've been injured and need a battle-tested partner to review your evidence, contact our team today to start your roadmap to recovery.

Partnering with The Todd Law Group, PLLC for Total Restoration

Choosing an advocate is the final and most critical step in your recovery roadmap. When you pursue an uninsured motorist claim Houston, you aren't just filing paperwork; you're challenging a corporate system designed to minimize its own losses. The Todd Law Group, PLLC brings a unique advantage to this struggle. Jeff Todd, licensed in Texas since 1994, transitioned from high-stakes corporate law to dedicated personal advocacy. This background means he understands the intellectual rigor required to dismantle the defense strategies used by major insurance carriers. We apply a sophisticated litigation approach to ensure your provider honors the full value of the policy you've paid for.

Our firm's presence in Houston, Austin, and Galveston reflects our deep commitment to the local community. We treat every client as a partner, providing the steady reassurance needed during a legal crisis. By combining the precision of a corporate legal hub with the compassion of a local practice, we offer a versatile specialist approach that prioritizes your total restoration. You shouldn't have to settle for a factory-style firm when your physical and financial health are on the line.

Beyond the Settlement: Our Holistic Approach to Personal Injury

We view legal representation as a vital component of a larger healing process. The Todd Law Group, PLLC coordinates with medical experts to ensure you receive care from high-caliber specialists right here in Houston. We emphasize reaching "maximum medical improvement" before discussing final settlement numbers, as this ensures your long-term needs are fully funded and accounted for. If your injury occurred on a commercial property or due to a hidden hazard, our insights into Premises Liability Law in Texas can provide further clarity on property owner responsibility and additional avenues for recovery.

Contingency-Based Advocacy: No Upfront Costs for Houston Families

We believe that financial distress should never be a barrier to justice. Our firm operates on a contingency-based model, meaning we don't collect a fee unless we win your case and recover money for you. The Todd Law Group, PLLC covers all upfront litigation expenses, including the costs for expert witnesses and accident reconstruction, so you can focus on your recovery without added financial strain. If you're ready to secure a stable partner for your journey, contact Jeff Todd for a free consultation today. We are dedicated to your holistic restoration from the moment we take your case until your health and stability are fully reclaimed.

Secure Your Path to Total Restoration

Navigating the aftermath of a collision with an uninsured driver is a complex legal journey that requires more than just filling out forms. You've learned that the 24-hour reporting rule for hit-and-runs is a critical deadline and that your own insurance company may prioritize its bottom line over your recovery. Successfully managing an uninsured motorist claim Houston involves a strategic roadmap that combines meticulous evidence gathering with a deep understanding of Texas UM/UIM statutes. It's about ensuring that a single moment of negligence doesn't dictate your financial future.

Jeff Todd has been licensed in Texas since 1994 and applies elite corporate rigor to every personal injury case. Our firm's holistic approach ensures that your physical healing and financial stability are treated with equal importance. We operate on a contingency-based model, meaning there's no recovery, no fee. You don't have to face the insurance giants alone or settle for a lowball offer that ignores your long-term needs. Schedule your free, confidential consultation with Jeff Todd today to begin your journey toward a total recovery. We're committed to standing by your side until your health and peace of mind are fully restored.

Frequently Asked Questions

What happens if I'm hit by an uninsured driver in Houston and it was a hit-and-run?

If you're the victim of a hit-and-run in Houston, your incident is legally categorized as an uninsured motorist claim. You must file a police report within 24 hours of the collision to preserve your right to seek compensation. This report serves as the formal record that an unidentified driver caused your damages. Without it, your insurance carrier may deny the claim based on a lack of verifiable evidence.

Will filing an uninsured motorist claim raise my insurance rates in Texas?

Filing a UM claim in Texas should not result in an increase to your insurance premiums. Texas law protects policyholders by prohibiting insurers from raising rates for accidents where the claimant was not at fault. Since an uninsured motorist claim Houston is based on the negligence of another party, your company cannot legally penalize you for utilizing the coverage you've faithfully paid for.

How long do I have to file a UM claim in Houston?

You generally have four years to file a lawsuit for an uninsured motorist claim in Texas. While standard personal injury lawsuits have a two-year statute of limitations, a claim against your own insurer is technically a breach of contract matter. However, you should still notify your insurance company as soon as possible to comply with your policy's specific reporting requirements and avoid unnecessary delays.

Can I sue an uninsured driver personally if they have no assets?

While you have the legal right to sue an uninsured driver personally, it's often a futile effort if they lack significant assets. Most individuals driving without insurance don't have the financial resources to pay a court-ordered judgment. Pursuing a claim through your own UM/UIM policy is almost always the most efficient and reliable way to secure a meaningful financial recovery for your injuries.

Do I need a lawyer for a UM claim if my insurance company is being 'nice'?

You should consult a lawyer even if your insurance adjuster seems helpful and cooperative. Their primary responsibility is to minimize the company's financial exposure, not to ensure you receive a maximum payout. A seasoned advocate can identify hidden policy benefits and prevent you from accepting a settlement that fails to cover the full scope of your future medical care.

What is the 'physical contact' rule for hit-and-run claims in Texas?

The "physical contact" rule in Texas requires that the unidentified vehicle actually touch your car to qualify for UM coverage. This regulation is designed to prevent fraudulent claims involving "phantom vehicles" that allegedly caused an accident without making contact. If there was no impact, your insurance company will likely deny the claim unless there is significant third-party witness testimony to corroborate your story.

How much is the average settlement for an uninsured motorist claim in Houston?

There is no universal "average" settlement because every case depends on specific policy limits and the severity of the victim's injuries. Your recovery is typically capped by the UM limits you selected when purchasing your policy, such as the $30,000 state minimum. Our focus is on maximizing these limits to ensure your medical bills and lost wages are fully addressed through a strategic legal approach.

Can I use my health insurance for car accident injuries if the other driver is uninsured?

You can use your personal health insurance to cover immediate medical costs, but your provider may have a right to be reimbursed from your eventual settlement. This process is known as subrogation. It's often more beneficial to work with medical specialists who are experienced in car accident recovery, as they can help coordinate billing in a way that protects your final financial restoration.